Subduing the Enemy Without Fighting: Sanctions and the Limits of Financial Network Power

The power of modern sanctions rests on the uneven structure of global financial networks. A small number of states sit at the financial and technological nexus of the global economy, exploiting chokepoints with relative ease. In what Henry Farrell and Abraham Newman call “weaponized interdependence,” states that control key financial networks can monitor transactions and deny access, turning global connectivity into leverage. Since the outset of the Cold War, the United States has increasingly relied on financial sanctions as a tool of statecraft. The expansion of dollar clearing surveillance, financial messaging systems, and regulatory enforcement since the 1990s has made sanctions easier to deploy and harder to evade. After Russia invaded Ukraine in 2022, the United States’ sanctions designations surged from 743 in 2021 to more than 2,200 in 2022, and exceeded 2,300 in 2023.

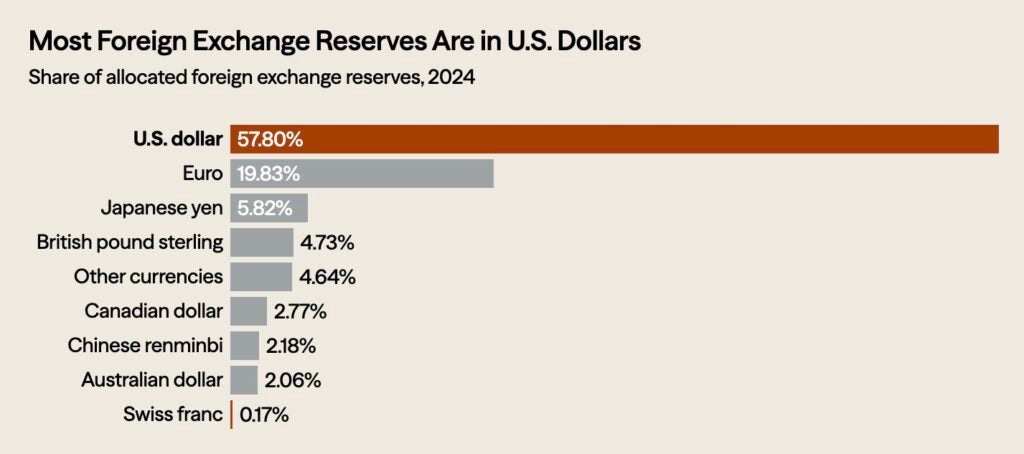

This escalation, however, has accelerated defensive adaptation from states on the receiving end of the economic stick. States exposed to financial chokepoints, including Russia and the People’s Republic of China (PRC), have invested in alternative payment systems, bilateral local currency settlement, and reserve diversification. These efforts have not displaced dollar dominance, but have incrementally weakened it. The U.S. dollar still accounts for 58 percent of global foreign exchange reserves and is involved in 89 percent of foreign exchange trades. Conversely, the RMB represents just 2.88 percent of global payments. Even so, incremental insulation reduces the transparency and connectivity of global financial networks, meaning fewer transactions flow through centralized channels. This reduced dependence on Western financial infrastructure, over time, may weaken the foundations that make economic coercion effective in the first place.

This dependence is rooted in the hierarchical nature of global financial networks, where transactions flow through a dense web of correspondent banking relationships that typically clear in dollars and pass through U.S. jurisdiction. Major payment messaging systems facilitate cross-border transfers by connecting thousands of financial institutions: the SWIFT Network (Society for Worldwide Interbank Financial Telecommunication) links more than 11,000 financial systems from over 200 territories and countries. The concentration of standardized messaging systems and correspondent banks provides both visibility and control. Hub states can monitor transactions that pass through their systems and deny access to actors deemed noncompliant with international or regional sanctions. Peripheral actors, by contrast, rely on continued access to these nodes for trade, investment, and capital flows.

Russia: Sanctions Shock and Rapid Financial Adaptation

Russia’s response to sanctions can be understood in three stages: an initial sanctions shock, rapid financial adaptation, and the structural limits of that adaptation. Russia’s exclusion from the majority of the global financial system in 2022 reflects the operational logic of the U.S.-led financial system. The United States, alongside its allies, restricted several major Russian banks, such as Vnesheconombank, from SWIFT messaging channels, limiting access to international financial communications and narrowing dollar clearing channels. In the months following its invasion of Ukraine, international sanctions designations expanded rapidly, targeting Russian financial institutions, state enterprises, and individuals. Secondary sanctions extended risk beyond Russia’s borders by threatening third-party banks and firms that facilitated restricted transactions. The intent of this uptick was not merely to signal disapproval, but to impose material constraints by exploiting Russia’s dependence on infrastructure located outside its sovereign control.

The combined U.S. and EU demonstration of network leverage exposed the vulnerability inherent in reliance on centralized financial architectures. For Moscow, insulation shifted from a hypothetical goal to an urgent necessity. To assert financial sovereignty, Russia expanded the use of its domestic financial messaging system, the System for Transfer of Financial Messages (SPFS), and increased its use of bilateral local currency settlement, particularly with China. This system provides an alternative channel for financial messaging when access to SWIFT is restricted. Russia has also accelerated local currency settlement, with between 90 and 99 percent of bilateral trade with the PRC is being conducted in rubles (RUB) and yuan (RMB) rather than dollars or euros.

These measures do not constitute a true alternative to the U.S.-led global financial system. SPFS remains modest relative to the scale of established networks with wider jurisdictions; much of its traffic remains domestic. More importantly, bilateral currency settlement may reduce exposure to dollar clearing restrictions, but it does not create a new universal medium of exchange—an advantage held by more entrenched global networks. Russia’s response reflects the necessity to adapt under constraint.

The PRC: Preemptive Insulation from Financial Chokepoints

The PRC’s adaptation differs from Russia’s in timing, but not direction. Beijing has not faced comprehensive sanctions in the same way Russia has. However, it has observed Russia’s vulnerability since 2022, as well as the expansion of U.S. export controls in advanced technology sectors. These measures reinforced Beijing’s perception that access to Western-controlled financial and technological networks could become a strategic vulnerability.

In response to U.S. export controls on AI technology, advanced semiconductors, and chip-making equipment, the PRC has invested in alternative financial infrastructure that reduces exposure to trade barriers. The Cross-Border Interbank Payment System (CIPS), a People’s Bank of China-backed system for cross-border payments in RMB, has expanded steadily since 2019. It has grown in both participant numbers and transaction volume in recent years, with the number of transactions tripling between 2020 and 2024. The volume of transactions passing through CIPS in 2024 alone increased by 43 percent. Rather than separate developments, the expansion of U.S. export controls has directly reinforced Beijing’s efforts to reduce reliance on Western financial systems, accelerating investment in alternatives such as CIPS.

Most global RMB transactions still rely on established messaging channels, and CIPS remains intertwined with the existing financial architecture. The majority of CIPS participants hail from Asia, accounting for 73 percent of transactions. Behind Asia are European institutions accounting for 17 percent, Africa for 4 percent, and North and South America each with 2 percent.

However, the limits of RMB internationalization are evident: it ranks just sixth among global payment currencies behind the U.S. Dollar, the Euro, the British Pound, Japanese Yen, and Canadian Dollar. Reserve composition has shifted gradually over the past decade, but no alternative currency approaches the scale or liquidity of the dollar. Assertions of imminent de-dollarization do not reflect the current global financial market, but they do reflect a strategic shift toward insulation from U.S.-centered financial power.

Source: Council of Foreign Relations, 2023

How Coercive Networks Erode ‘Weaponized Interdependence’

Still, it would be naive to dismiss adversarial developments toward disconnected financial sovereignty as merely symbolic. The PRC and Russia have expanded bilateral currency settlement and RMB-denominated trade, while the BRICS bloc has promoted lending and transactions in domestic currencies through institutions such as its New Development Bank. While still in early stages, these steps reflect a shared effort among some states to reduce exposure to dollar-centered infrastructure.

This logic extends beyond adversaries and sanctioned states. Since secondary sanctions extend to third parties, financial institutions in neutral countries must weigh access to dollar clearing against continued engagement with sanctioned actors. For instance, India risked secondary sanctions by continuing Russian oil purchases and financial transactions with U.S.-sanctioned Russian banks after 2022. This pressure reinforces the centrality of U.S. financial statecraft. However, third-party countries are increasingly exploring alternative channels to reduce that dependence.

Economic coercion, therefore, produces a dual effect. In the short term, concentrated networks amplify leverage for the states already in control of the system, the United States and its allies. In the medium- to long-term, repeated use of that leverage encourages vulnerable states to diversify reserves, expand local currency trade, and invest in parallel infrastructure. Each adaptation may appear marginal, but collectively, they have the potential to alter the structure of the U.S.-backed financial network.

Coercive power also depends on network density. The more transactions pass through centralized nodes such as SWIFT, the greater the visibility and the more powerful economic sticks will be. As such, diversification erodes coercive power. Parallel messaging systems reduce transparency, bilateral currency settlements limit correspondent banking oversight, and reserve diversification reduces reliance on a single currency. None of these changes eliminate dollar dominance. They do, however, incrementally reduce the share of global activity subject to centralized monitoring and restriction.

This tradeoff is already visible in recent policy decisions. On April 17, the Treasury Department issued General License 134B and allowed Russian-origin crude oil that had already been loaded onto vessels to reach its destination. In a hearing before the Financial Services and General Government Subcommittee on the House Appropriations Committee, Secretary Scott Bessent explained that the Treasury extended the general license to avoid pulling oil supply off the market overnight and driving up global prices. A sudden disruption would have raised costs for U.S. partners and strained already tight energy markets. That decision carries a cost. The license allows revenue from those shipments to flow back to Russia and softens the immediate impact of sanctions. It also signals to buyers and intermediaries that the United States will adjust enforcement when market pressure rises. That expectation weakens the force of future restrictions. Sanctions can impose costs, but they cannot do so without regard for the system they operate in.

These dynamics do not imply that sanctions are ineffective or strategically misguided. Despite inefficiencies and unintended consequences, sanctions remain a vital signaling tool in the foreign policy toolkit. Echoing Sun Tzu’s centuries-old strategic ideal to “subdue the enemy without fighting,” financial coercion remains one of the few tools available to impose costs without direct military escalation.

The Strategic Tradeoff of Network Power

The strategic question is not whether economic coercion works, but how repeated reliance on it reshapes the network structures that make it possible. Weaponized interdependence demonstrates the power of hub states in a densely interconnected system and reveals the target’s vulnerability. When peripheral actors perceive a persistent risk of exclusion, they seek insulation. Over time, insulation changes the topography of the network. A system once characterized by concentrated hubs may evolve towards a looser configuration with more regional and bilateral channels.

Rather than a contradiction, this presents a tension for the United States. Network centrality is a competitive advantage. Exercising that advantage reinforces deterrence and constrains adversaries. Yet the more frequently and broadly that leverage is deployed, the stronger the incentive for states on the receiving end to construct alternatives. The resulting erosion may not displace the dollar or dismantle existing institutions, but may instead produce a weaker, less transparent system in which fewer transactions flow through centralized nodes.

Fragmentation in response to the post-2022 surge in sanctions remains partial and uneven, but it is already weakening the network structures that sustain U.S. leverage. Preserving that advantage will require restraint as well as resolve. Without it, the United States risks undermining the very system on which its economic power depends.

Views expressed are the author’s own and do not represent the views of GSSR, Georgetown University, or any other entity. Image Credit: Brookings